Serkan Zeytun, Ph.D.

Department of Financial Mathematics

October 2012

Supervisor: Ömür Uğur (Institute of Applied Mathematics, Middle East Technical University, Ankara)

Co-supervisor: Ralf Korn (Department of Mathematics, University of Kaiserslautern, Germany)

Abstract

In this thesis we mainly focused on the usage of the Conditional Value-at-Risk (CVaR) in risk management and on the pricing of the arithmetic average basket and Asian options in the Black-Scholes framework via a new log-normal sum approximation method. Firstly, we worked on the linearization procedure of the CVaR proposed by Rockafellar and Uryasev. We constructed an optimization problem with the objective of maximizing the expected return under a CVaR constraint. Due to possible intermediate payments we assumed, we had to deal with a re-investment problem which turned the originally one-period problem into a multiperiod one. For solving this multi-period problem, we used the linearization procedure of CVaR and developed an iterative scheme based on linear optimization. Our numerical results obtained from the solution of this problem uncovered some surprising weaknesses of the use of Value-at-Risk (VaR) and CVaR as a risk measure.

In the next step, we extended the problem by including the liabilities and the quantile hedging to obtain a reasonable problem construction for managing the liquidity risk. In this problem construction the objective of the investor was assumed to be the maximization of the probability of liquid assets minus liabilities bigger than a threshold level, which is a type of quantile hedging. Since the quantile hedging is not a perfect hedge, a non-zero probability of having a liability value higher than the asset value exists. To control the amount of the probable deficient amount we used a CVaR constraint. In the Black-Scholes framework, the solution of this problem necessitates to deal with the sum of the log-normal distributions. It is known that sum of the log-normal distributions has no closed-form representation. We introduced a new, simple and highly efficient method to approximate the sum of the log-normal distributions using shifted log-normal distributions. The method is based on a limiting approximation of the arithmetic mean by the geometric mean. Using our new approximation method we reduced the quantile hedging problem to a simpler optimization problem.

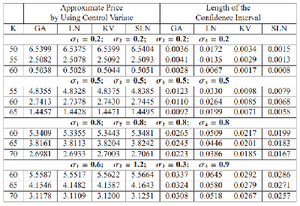

Our new log-normal sum approximation method could also be used to price some options in the Black-Scholes model. With the help of our approximation method we derived closed-form approximation formulas for the prices of the basket and Asian options based on the arithmetic averages. Using our approximation methodology combined with the new analytical pricing formulas for the arithmetic average options, we obtained a very efficient performance for Monte Carlo pricing in a control variate setting. Our numerical results show that our control variate method outperforms the well-known methods from the literature in some cases.

Keywords: Risk measures, linearization of conditional value-at-risk, quantile hedging, pricing options based on arithmetic averages, variance reduction with control variates