Abdulwahab Animoku, Ömür Uğur, Yeliz Yolcu-Okur, Modeling and Implementation of Local Volatility Surfaces in Bayesian Framework, Computational Management Science, 15(2): pp. 239 - 258 (June 2018).

Abstract

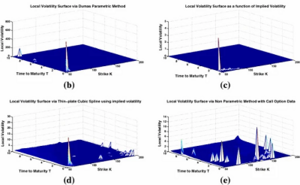

In this study, we focus on the reconstruction of volatility surfaces via a Bayesian framework. Apart from classical methods, such as, parametric and non-parametric models, we study the Bayesian analysis of the (stochastically) parametrized volatility structure in Dupire local volatility model. We systematically develop and implement novel mathematical tools for handling the classical methods of constructing local volatility surfaces. The most critical limitation of the classical methods is obtaining negative local variances due to the ill-posedness of the numerator and/or denominator in Dupire local variance equation. While several numerical techniques, such as Tikhonov regularization and spline interpolations have been suggested to tackle this problem, we follow a more direct and robust approach. With the Bayesian analysis, choosing a suitable prior on the positive plane eliminates the undesired negative local variances.

Keywords: Local volatility model, Bayesian analysis, Tikhonov regularization