Abdulwahab Animoku, Ph.D.

Department of Financial Mathematics

September 2018

Supervisor: Ömür Uğur (Institute of Applied Mathematics, Middle East Technical University, Ankara)

Abstract

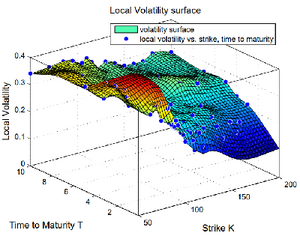

In this thesis, we investigate and implement advanced methods to quantify uncertain parameter(s) in Dupire local volatility equation. The advanced methods that will be investigated are Bayesian and stochastic Galerkin methods. These advanced techniques implore different ideas in estimating the unknown parameters in PDEs. The Bayesian approach assumes the parameter is a random variable to be sampled from its posterior distribution. The posterior distribution of the parameter is constructed via “Bayes theorem of inverse problem”. Stochastic Galerkin method involves propagating uncertainty into a deterministic input parameter and then quantifying the randomness in the solution. In addition, the performance and numerical analysis of each approach will be studied.

Keywords: Local volatility, Bayesian analysis, Stochastic Galerkin method, Tikhonov regularization