Caner Karakurt, Ph.D.

Department of Financial Mathematics

June 2025

Supervisor: Ömür Uğur (Institute of Applied Mathematics, Middle East Technical University, Ankara)

Co-Supervisor: Alper Ali Hekimoğlu (European Investment Bank, Luxembourg)

Abstract

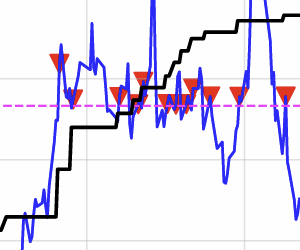

This study develops an optimal pairs trading strategy based on the inhomogeneous geometric Brownian motion (IGBM) process. The proposed model aims to identify an upper boundary that maximizes the expected return of the strategy, given a predetermined lower boundary. Compared to well-known processes such as Ornstein-Uhlenbeck and Cox-Ingersoll-Ross, the IGBM process has received significantly less attention in the academic literature. In this research, we derive an analytical expression for the value function associated with the strategy. The theoretical analysis is validated through simulation studies and, empirical back-testing results provide strong evidence supporting the model’s profitability. The primary contribution of this study lies in deriving an explicit solution for the analytical value function of the pairs trading strategy and determining the optimal upper boundary within the framework of the IGBM process.

Keywords: Pairs trading, inhomogeneous geometric Brownian motion, optimal boundary, value function